Luxembourg capitalisation contract

What is the Luxembourg Security Triangle, this mechanism for protecting savers?

Alexandre Juve

Founder, Epargne Plurielle

What is the Luxembourg Security Triangle, this saver protection mechanism?

Life insurance contracts combine many advantages, including capital security, ease of wealth transfer, and a very wide choice of investment options.

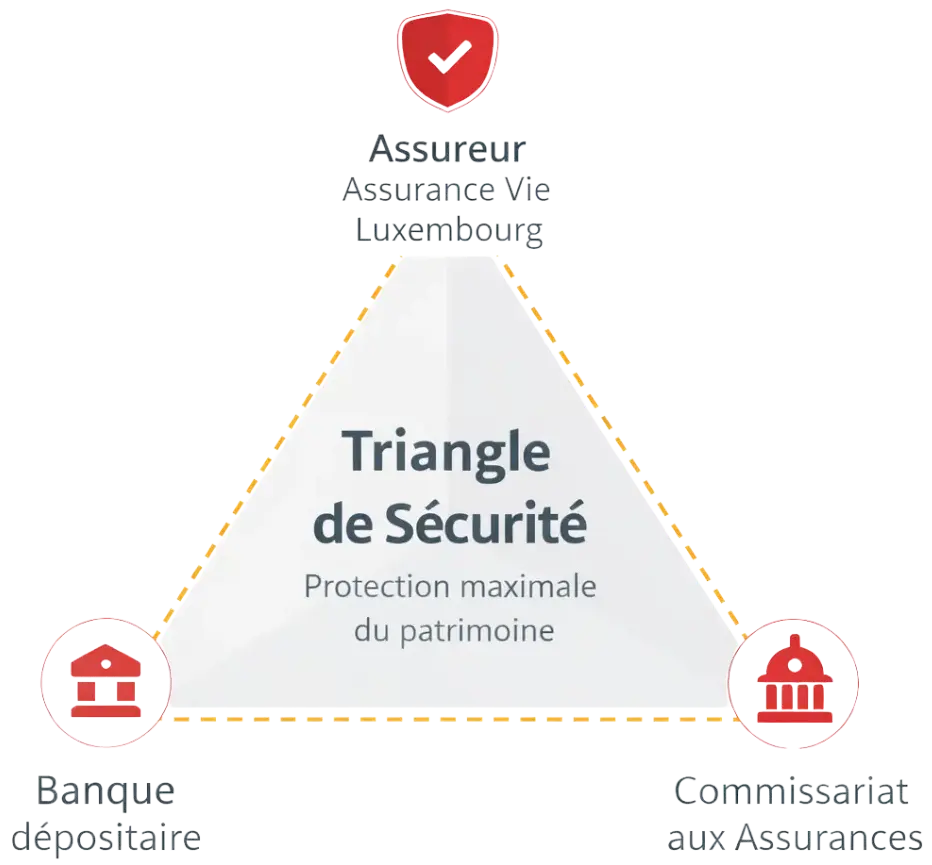

Characterised by a very high level of security and transparency for the policyholder, Luxembourg life insurance contracts are governed by the regulations of the Grand Duchy, which are unique in Europe. They require the signing of a tripartite agreement between the custodian bank, the insurance company, and the Luxembourg insurance supervisory authority (Commissariat aux assurances), hence the term “security triangle”.

The Luxembourg Security Triangle, a unique protection regime, ensures the legal and physical separation between policyholders’ assets on the one hand and the assets of the company’s shareholders and other creditors on the other. This framework differs from the French system, particularly in the event of exceptional measures such as the Sapin 2 law.

The assets linked to life insurance contracts, called technical provisions, are deposited with a custodian bank previously approved by the Commissariat aux Assurances, but separated from the company’s other liabilities.

To provide even greater security for your capital, the segregation of assets is checked every quarter by the Commissariat aux Assurances. In the event of the insurer’s default, the supervisory authority has the possibility to block the accounts in order to protect the rights of policyholders. The concrete consequences of this protection mechanism can be seen in our comparison of Luxembourg life insurance policies, which puts into perspective the main contracts benefiting from the security triangle.

The super privilege, priority over all other creditors.

In addition, there is the “super privilege”, which grants beneficiaries a first-ranking privilege. Indeed, insurance companies give them priority over all other creditors of the company, whoever they may be, even if it is the State.

This privilege therefore allows holders of a Luxembourg life insurance policy to recover 100% of their claims as a priority in the event of the insurance company’s default.

How the security triangle works in practice in the event of default.

In the event of the default of a Luxembourg insurer, the main objective is not to compensate through a capped guarantee, but to legally and operationally protect the rights of policyholders.

The assets linked to life insurance contracts, called technical provisions, are deposited with an independent custodian bank and strictly segregated, meaning they cannot be mixed with the insurer’s own assets.

In this type of situation, the Commissariat aux Assurances may decide to freeze the accounts linked to the technical provisions in order to prevent any unauthorized outflow of assets. The priority is then to organize an orderly restitution of the assets for the benefit of policyholders.

In Luxembourg, this restitution is generally made in kind: the aim is to recover the assets held within the contract, at their value at the time of restitution. The security triangle therefore protects a legal framework and a priority ranking, but does not eliminate market fluctuations.

What the security triangle protects… and what it does not protect.

The security triangle primarily protects a structure: the segregation of assets, regulatory supervision, and the priority of policyholders over other creditors.

However, it is essential to understand its limits:

| Protects | Does not protect |

|---|---|

| Legal and physical segregation of assets | Investment performance |

| Legal priority of policyholders (super privilege) | Allocation errors or lack of diversification |

| Strict regulatory framework and ongoing supervision | The restoration of lost economic value |

| Ring-fencing of technical provisions | Immediate liquidity in the event of exceptional proceedings |

The security triangle is therefore a legal and operational protection mechanism. It strengthens the security of the framework, but does not replace analysis of the investment vehicles or the rigorous selection of partners.

Who the security triangle is really intended for

The security triangle is primarily intended for investors seeking a robust framework to structure significant wealth over the long term.

It is particularly relevant for:

business owners and liberal professions,

investors with substantial financial wealth,

individuals exposed to several jurisdictions or currencies,

profiles sensitive to the legal protection of capital.

However, it is generally not suitable for savers with modest amounts or those primarily seeking a simple and standardized solution. The security triangle is not a “mass-market” product, but a demanding wealth structuring tool.

Benefit from independent advice tailored to your situation.

Contact an independent Luxembourg life insurance specialist.

Submit your request via the form below. It is quick, confidential, and without obligation.